14 February 2021 — Michael Roberts Blog

Michael Roberts

During the year of the COVID, global consumer and producer prices dropped fell. In some manufacturing-based economies, there was even a fall in price levels (deflation) eg the Euro area, Japan and China).

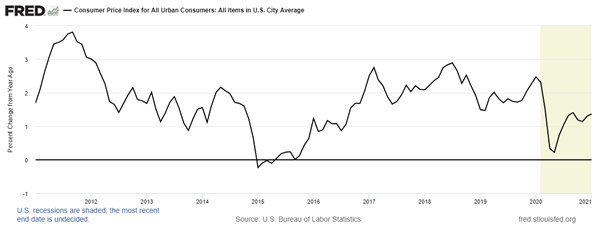

US inflation rate (annual %)

“Effective demand” as Keynesians like to call it, plummeted, with business investment and household consumption dropping sharply. Savings rates rose to high levels (both corporate savings relative to investment and household savings).

Household savings rates (% of income) – OECD

| Country | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| United Kingdom | 3.1 | 3.6 | 4.9 | 2.2 | 0.0 | 6.1 | 6.5 | 19.4 |

| United States | 6.6 | 7.6 | 7.9 | 7.0 | 7.2 | 7.8 | 7.5 | 16.1 |

| Euro area (16 countries) | 5.6 | 5.7 | 5.7 | 5.7 | 5.6 | 6.4 | 6.7 | 14.3 |

Many companies went bust and many lower income households either lost their jobs or faced reductions in wages. Higher income households maintained their wage levels, but they were unable to travel or spend on leisure and entertainment.

But now, as the rollout of vaccines accelerates across the advanced economies and governments and central banks continue to inject credit money and direct funding for business and households, the wide expectation is that the major economies will make a fast recovery in investment, spending and employment – at least by the second half of 2021.

Now the concern is that, instead of a continued slump, there is a risk of ‘overheating’ in the major economies, causing an inflation of prices generated by ‘too much’ government spending and continued ‘loose’ monetary policy.

The UK’s Financial Times echoed the voices of leading mainstream American Keynesian economists that “a strong recovery and sizeable stimulus raise the possibility of the US ‘overheating’”. Former treasury secretary Larry Summers and former IMF chief economist Oliver Blanchard both warned that the passing by the US Congress of the proposed $1.9tn spending package, on top of last year’s $900bn stimulus, risked inflation.

Summers argued that the size of the spending package, about 9 per cent of pre-pandemic national income, would be much larger than the estimate of the shortfall in economic output from its ‘potential’ by the Congressional Budget Office (CBO). That, combined with loose monetary policy, the accumulated savings of consumers who have been unable to spend and already-falling unemployment could contribute to mounting inflationary pressure. ‘Pent-up demand’ would explode, leading to 1970s-type inflation. “There is a chance that macroeconomic stimulus on a scale closer to World War II levels than normal recession levels will set off inflationary pressures of a kind we have not seen in a generation,” said Summers.

Summers’ view must be taken with the proverbial pinch of salt, considering that in April last year, he argued that the COVID pandemic would be merely a short sharp decline, somewhat like tourist areas (Cape Cod in his case) closing down for the winter, and the US economy would come roaring back in the summer. Two things blew that forecast out of the Atlantic: first, the winter wave of COVID (actually in the case of the US, because of lax lockdowns etc, the spring wave just continued); and second, hundreds of thousands of small businesses (and some larger ones) went bust and so business was not able to return to normal after the ‘winter break’.

Summers’ argument is also based on some very dubious economic categories. He measured the fiscal and monetary stimulus being applied by Congress and the Fed in 2021 against the “potential output” of the economy. This is a supposed measure of the maximum capacity of investment and spending that an economy could achieve with ‘full employment’ without inflation. The category is so full of holes, that economists come up with different measures of ‘potential output’, which anyway seems to be a moveable feast depending on productivity and employment growth and likely investment in new capacity.

Larry Summers reckons the Biden relief package will inject around $150 billion per month, while CBO says the monthly gap between actual and potential GDP is now around $50 billion and will decline to $20 billion a month by year-end (because the CBO assumes the COVID-19 virus and all its variants will be under control).

Former New York Fed President Bill Dudley backed up Summers in arguing that Four More Reasons to Worry About US Inflation. First, economic slumps brought on by pandemics tend to end faster than those caused by financial crises. This is Summers’ Cape Cod argument revived. And second, “thanks to rescue packages and a strong stock market, household finances are in far better shape now than they were after the 2008 crisis.” You might ask whether a rocketing stock market benefits the 93% of Americans who have no stock investments (or large pension funds). And while the better-paid may have increased savings to spend, that is not the case for lower to middle income earners. Dudley also claimed that companies have “plenty of cash to spend and access to more at low interest rates”. Again, he seems to concentrate on the large techs and finance firms that are hoovering up government money and stock market gains. Meanwhile there are hundreds of thousands of smaller companies which are on their knees and in no position to launch a big investment plan even if they can get loans at low rates. The number of these zombie companies are growing by the day.

It’s true as Dudley says that ‘inflation expectations’ are rising and that can be a good indicator of future inflation – if households think prices are going to rise, they tend to start spending in advance and so stimulate price rises – and vice versa. And it’s also true that, given the sharp fall in price inflation at the start of the pandemic lockdowns last year, any recovery in prices now will show up as a statistical year on year rise. But as you can see from this graph below inflation expectations are hardly at a level of “of a kind we have not seen in a generation” (Summers).

The other worry of the ‘inflationists’ is that the US Fed will generate an inflationary spiral through its ‘lax’ monetary policies. The Fed continues to plough humungous amounts of credit money into the banks and corporations and also has weakened its inflation target of 2% a year to a 2% average inflation over some undefined period. Thus, the Fed will not hike interest rates or cut back on ‘quantitative easing’ even if the annual inflation rate heads over 2%.

Fed chair Jay Powell made it clear in a recent speech to the Economic Club of New York (business people and economists) that the Fed had no intention of reining in its monetary easing. Powell even gave a date – no tightening of policy before 2023. This has upset the anti-inflation theorists. Gillian Tett in the FT put it: “the Fed has now taken this so-called “forward guidance” to a new level that seems dangerous. He should puncture assumptions that cheap money is here indefinitely, or that Fed policy is a one-way bet. Otherwise his attempts to ward off the ghosts of 2013 will eventually unleash a new monster in the form of a bigger market tantrum, far more damaging than last time — especially if investors have been lulled into thinking the Fed will never jump.”

The FT itself went on: “The Fed’s pledge to leave policy on hold until 2022, however, risks undermining its credibility: it cannot promise to be irresponsible. … it must watch out for any sign that inflation expectations are rising and respond to the data rather than tie itself to the mast.” Dudley echoed this view. “If the Fed does not tighten when inflation appears, it might have to reverse course quickly if it starts getting out of hand. That, in turn, could set off market fireworks.”

But are the inflationists’ warnings valid? First, they are really based on a quick and significant ‘Cape Cod’ economic recovery. But the pandemic is not over yet and the vaccines have not been rolled out to any level to suppress the virus sufficiently yet. What if the new variants that are beginning to circulate are resistant to existing vaccines so that a new ‘wave’ emerges? A summer recovery could be delayed indefinitely.

Moreover, these inflation forecasts are based on two important theoretical errors, in my view. The first is that the huge injections of credit money by the Fed and other central banks that we have seen since the global financial crash in 2008-9 have not led to an inflation of consumer prices in any major economy even during the period of recovery from 2010 onwards – on the contrary (see the US inflation graph above), US inflation rates have been no more than 2% a year and they have been even lower in the Eurozone and Japan, where credit injections have also been huge.

Instead, what has happened has been a surge in the prices of financial assets. Banks and financial institutions, flooded with the generosity of the Fed and other central banks, have not lent these funds onwards (either because the big companies did not need to borrow or the small ones were to risky to lend to). Instead, corporations and banks have speculated in the stock and bond markets, and even borrowed more (through corporate bond issuance) given low interest rates, paying out increased shareholder dividends and buying back their own shares to boost prices. And now with the expectation of economic recovery, investors poured a record $58bn into stock funds, slashing their cash holdings and also piled $13.1bn into global bond funds while pulling $10.6bn from their cash piles.

So Fed and central bank money has not caused in inflation in the ’real economy’ which continued to crawl along at 2% a year or lower in real GDP growth, while the ‘fictitious’ economy exploded. It is there that inflation has taken place.

This is where the ’Austrian school’ of economics comes in. They see this wild expansion of credit leading to ‘malinvestment’ in the real economy and eventually to a credit crunch that hits the productive sectors of the ‘pure’ market economy. This view is expressed by that bastion of conservative economics, the Wall Street Journal. So while the Keynesians worry about overheating and inflation in true 1970s style, the Austrians worry about a credit/debt implosion.

In contrast, the exponents of Modern Monetary Theory (MMT) are quite happy about the Fed injections and the government stimulus programs. Modern Monetary Theory exponent Stephanie Kelton, author of The Deficit Myth, when asked whether she was worried about the stimulus bill causing inflation, said: “Do I think the proposed $1.9 trillion puts us at risk of demand-pull inflation? No. But at least we are centering inflation risk and not talking about running out of money. The terms of the debate have shifted.”

But neither the Keynesians, the Austrians nor the MMT exponents have it right theoretically, in my view. Yes, the Austrians are right that the expansions of credit money are driving up debt levels to proportions that threaten disaster if they should collapse. Yes, the MMT exponents are right that government spending per se, even if financed by central bank ‘printing’ of money will not cause inflation, per se. But what both schools ignore is what is happening to the productive sectors of the economy. If they do not recover then, fiscal stimulus won’t work and monetary stimulus will be ineffective too.

Take the proposed $1.9 trillion stimulus package. Even assuming the whole package is passed by Congress (increasingly unlikely) and then implemented, the stimulus is spread over years not months. Moreover, the paychecks to households will more likely end up being used to pay down debt, bump up savings and cover rent arrears and health care bills. There won’t be much left to go travelling, eat in restaurants and buy ‘discretionary’ items.

Moreover, as I have argued in many previous posts, the Keynesian view that government spending delivers a strong ‘multiplier’ effect on economic growth and employment is just not borne out by the evidence. Sure, government handouts to households and investment in infrastructure may generate a short boost to the economy. But raising government investment from 3% of GDP to 4% of GDP over five years or so cannot be decisive if business sector investment (about 15-20% of GDP) continues to stagnate. Indeed, as government debt grows to new highs (in the case of the US, to over 110% of GDP) even if interest rates stay low, interest costs to GDP for governments will rise and eat into funds available for productive spending. And with corporate debt also at record highs, there is no room for debt heavy corporations to cope with any reversal in low interest rates.

The problem is not inflationary ‘overheating’; it is whether the US economy can ever recover sufficiently to get close to ‘full employment’. The official US unemployment rate may be ‘only’ 6.7% but even the statistical authorities and the Fed admit that it’s probably more like 11-12% and even worse if you include the 2% of the labour force that has left the labour market altogether.

The problem is the profitability of the capitalist sector of the US economy. If that does not rise back to pre-pandemic levels at least (and that was near an all-time low), then investment will not return sufficiently to restore jobs, wages and spending levels.

Last year, G Carchedi and I developed a new Marxist approach to inflation. We have yet to publish our full analysis with evidence. But the gist of our theory is that inflation in modern capitalist economies has a tendency to fall because wages decline as a share of total value-added; and profits are squeezed by a rising organic composition of capital (ie more investment in machinery and technology relative to employees). This tendency can be countered by the monetary authorities boosting money supply so that money price of goods and services rise even though there is a tendency for the growth in the value of goods and services to fall.

During the year of the COVID, corporate profitability and profits fell sharply (excluding government bailouts and with the exception of big tech, big finance and now big pharma). Wage bills also fell (or to be more exact, wages paid to the many fell while some saw wages rise). These results were deflationary. But the central banks pumped in the money. US M2 money supply was up 40% in 2020. So US inflation, after dropping nearly to zero in the first half of 2020, moved back up to 1.5% by year end. Now if we assume that both profits and wages will improve by 5-10% this year and Fed injections continue to rise, then our model suggests that US inflation of goods and services will rise, perhaps to about 3% by end 2021 – pretty much where consumer expectations are going (see graph above).

That’s hardly ‘generation high’ inflation. And the view of Jay Powell and new Treasury Secretary Janet Yellen is “I can tell you we have the tools to deal with that (inflation) risk if it materializes.” Well, the US monetary and fiscal authorities may think they can control inflation (although the evidence is clear that they did not in the 1970s and have not controlled ‘disinflation’ in the last ten years). But they can do little to get the US economy onto a sustained strong pace of growth in GDP, investment and employment. So the US economy over the next few years is more likely to suffer from stagflation, than from inflationary ‘overheating’.

Leave a comment